The reality is

that the housing and mortgage market (for the time being) has shown a

noteworthy resilience. Indeed on the back of the Monetary Policy pursued by the

Bank of England there has been a notable improvement of macro-economic

conditions! In July for example it was announced that we are witness to the

lowest levels of unemployment for nearly 50 years. Furthermore,

despite the UK construction industry building 21% more properties than

same time the previous year, there has still been a disproportionate

increase in demand for housing, particularly in the most thriving areas of

the Country. Repossessions too are also at an all-time low at 3,985 for the

last Quarter (Q1 2017) from a high of 29,145 in Q1 2009. All these things have

resulted in...

Property values in Stoke-on-Trent according

to the

Land Registry are 3.1% higher than a year ago

So, what does

all this mean for the homeowners and landlords of Stoke-on-Trent, especially in

relation to property prices moving forward?

One vital bellwether of the

property market (and property values) is the mortgage market. The UK mortgage

market is worth £961,653,701,493 (that’s £961bn) and it representative of

13,314,512 mortgages

(interestingly, the UK’s mortgage market is the largest in Europe in terms of

amount lent per year and the total value of outstanding loans). Uncertainty causes

banks to stop lending – look what happened in the credit crunch and that

seriously affects property prices.

Roll the clock back to 2007, and nobody had heard of the

term ‘credit crunch’, but now the expression has entered our everyday

language. It took a few months

throughout the autumn of 2007, before the crunch started to hit the Stoke-on-Trent

property market, but in late 2007, and for the following year and half, Stoke-on-Trent

property values dropped each month like the notorious heavy lead balloon, meaning

…

The credit crunch caused Stoke-on-Trent property values to drop by 19.3%

Under

the sustained pressure of the Credit Crunch, the Bank of England realised that

the UK economy was stalling in the early autumn of 2008. Loan book lending

(sub-prime phenomenon) in the US and across the world was the trigger for this

pressure. In a bid to stimulate the British economy there were six successive

interest rates drops between October 2008 and March 2009; this resulted in

interest rates falling from 5% to 0.5%!

Thankfully,

after a period of stagnation, the Stoke-on-Trent property market started to

recover slowly in 2011 as certainty returned to the economy as a whole and Stoke-on-Trent

property values really took off in 2013 as the economy sped upwards. Thankfully,

the ‘fire’ was taken out of the property market in Spring 2015 (otherwise we could have had another boom and

bust scenario like we had in the 1960’s, 70’s and 80’s), with new mortgage

lending rules. Throughout 2016, we saw a return to more realistic and stable

medium term property price growth. Interestingly, property prices recovered in Stoke-on-Trent

from the post Credit Crunch 2009 dip and are now 17.2% higher than they were in

2009.

Now,

as we enter the summer of 2017, with the Conservatives having been re-elected

on their slender majority, the Stoke-on-Trent property market has recouped its

composure and in fact, there has been some aggressive competition among

mortgage lenders, which has driven mortgage rates down to record lows. This is

good news for Stoke-on-Trent homeowners and landlords, over the last few months

a mortgage price war has broken out between lenders, with many slashing the

rates on their deals to the lowest they have ever offered. For example, last month, HSBC launched a 1.69%

five-year fixed mortgage!

Interestingly,

according to the Council of Mortgage Lenders, the level of mortgage lending had

soared to an all-time high in the UK.

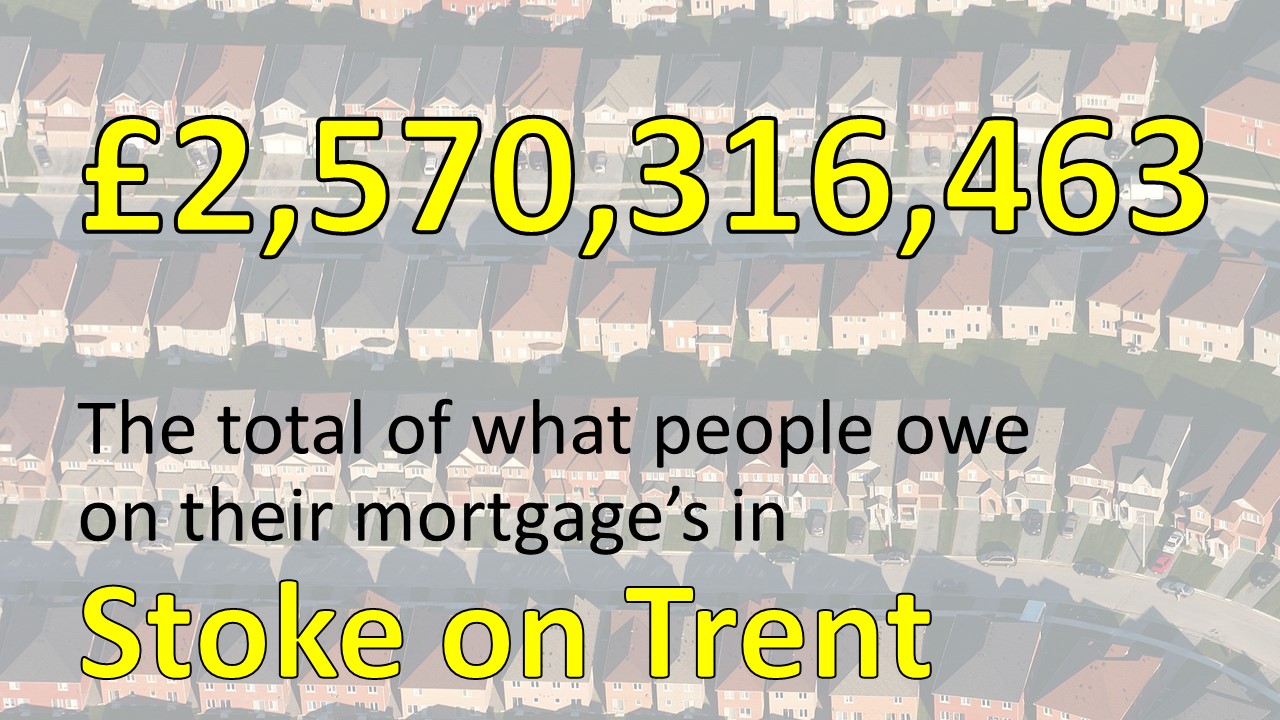

In the Stoke-on-Trent postcodes of ST1

to ST4, ST6 & ST9, if you added up everyone’s mortgage, it would total £2,570,316,463!

Since

1977, the average Bank of England interest rate has been 6.65%, making the

current 323 year all time low rate of 0.25% very low indeed. Thankfully, the

proportion of borrowers fixing their mortgage rate has gone from 31.52% in the autumn

of 2012 to the current 59.3%. If you haven’t fixed – maybe you should follow

the majority?

In

my modest opinion, especially if things do get a little rocky and uncertainty

seeps back in the coming years (and nobody knows what will happen on that

front), one thing I know is for certain, interest rates can only go one way

from their 300 year ultra 0.25% low level ... and that is why I consider it

important to highlight this to all the homeowners and landlords of Stoke-on-Trent.

Maybe, just maybe, you might want to consider taking some advice from a

qualified mortgage adviser? There are plenty of them in Stoke-on-Trent.

If you are interested in the Stoke-on-Trent

Property Market, please have a look at my other blogs on the subject, or give us a call on 01782 262880 for help and advice

No comments:

Post a Comment